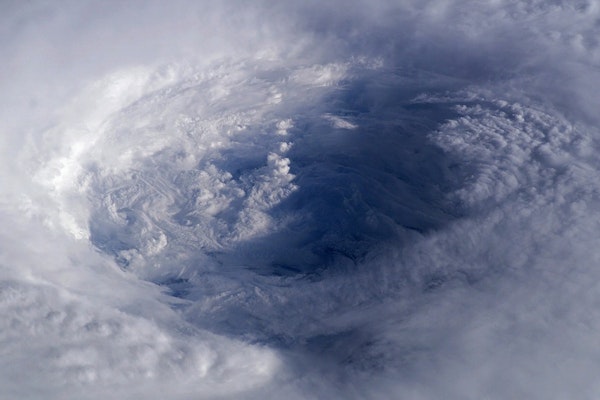

Private Hurricane Evacuation Service Offers Florida Residents Guaranteed Flights

A new Florida company is offering annual memberships that guarantee seats on chartered evacuation flights during hurricanes. The service raises questions about disaster preparedness, evacuation access, and how private solutions may reshape catastrophe response.

August 6

Catastrophe

Property

Risk Management

Florida

Georgia

Home Washer Leak Sparks $167K Insurance Subrogation Lawsuit Against LG

A Florida insurer alleges a defective LG washing machine caused extensive water damage and is seeking reimbursement through a product liability subrogation lawsuit. The case underscores the importance of origin and cause investigations and evidence preservation in property claims.

August 6

Litigation

Property

Subrogation

Florida

Why August Marks the Start of the Atlantic Hurricane Season’s Busiest Period

August brings warmer ocean waters, lower wind shear, and more tropical waves, creating conditions that favor hurricane development. Early August activity can also offer clues about how active the rest of the Atlantic season may become.

August 4

Catastrophe

Property

Risk Management

Florida

Georgia

North Carolina

South Carolina

Washington Wildfires Destroy More Than 600 Structures, Force 60,000 Evacuations

Multiple fast-moving wildfires remain 0% contained as evacuations continue across the Spokane region. Claims adjusters should prepare for significant residential, commercial, and infrastructure losses as damage assessments begin.

August 3

Catastrophe

Property

Risk Management

Washington

Final Defendant Sentenced in $6.6M Florida Insurance Fraud Scheme

A South Florida fraud scheme manipulated lender-placed homeowners insurance policies, resulting in $6.6 million in illicit gains. The final defendant received nearly four years in prison, closing a case that highlights vulnerabilities in insurance placement and premium disbursement.

August 3

Fraud

Insurance Industry

Litigation

Property

Florida

Burglars Use Instagram to Target Empty Homes as August Theft Claims Peak

Allstate says burglary claims reach their highest point in August as many travelers share their trips on social media. The trend highlights theft prevention, homeowners coverage limits, and documentation steps that can affect insurance claims.

August 3

Insurance Industry

Property

Risk Management

Technology

Triple-I: Wildfire Risk Expands Beyond the West as Heat Waves Drive US Fire Exposure

A new Insurance Information Institute brief says heat waves, drought and development in the wildland-urban interface are driving wildfire exposure beyond the Western United States, creating new underwriting and claims challenges for insurers.

August 3

Catastrophe

Legislation & Regulation

Property

Risk Management

Underwriting

California

Florida

Georgia

Nebraska

California’s $3.8 Billion Wildfire Technology Plan Aims to Reduce Insurance Losses

California is expanding satellites, AI camera networks, airtankers, and drone technology to detect wildfires earlier. State leaders hope reducing structure losses will help stabilize the homeowners insurance market and ease pressure on the FAIR Plan.

July 29

Catastrophe

Insurance Industry

Property

Risk Management

Technology

California

Hurricane Genevieve Sends Massive Surf to Southern California, Raising Coastal Damage Risks

Long-period swells from Hurricane Genevieve are expected to generate dangerous surf, rip currents, and localized coastal impacts across Southern California through the weekend, even without a direct landfall.

July 29

Catastrophe

Liability

Marine

Property

Risk Management

California

How Smart Glasses Are Transforming Insurance Claims and Field Inspections

AI-enabled smart glasses are helping insurers standardize inspections, improve documentation, reduce travel, and support remote claims handling while giving adjusters real-time guidance in the field.

July 27

Catastrophe

Property

Technology

Hurricane Fausto Forecast Raises Risk of Wind and Rain Impacts for Hawaii

The first hurricane to enter the Central Pacific Basin this season is expected to approach Hawaii early next week. Forecasters say confidence is growing that parts of the islands could see wind and rainfall impacts, though the exact track and intensity remain uncertain.

July 24

Catastrophe

Property

Risk Management

Hawaii

Texas Flood Recovery Begins After 135 Homes Are Destroyed in Kerr County

State officials say hundreds more homes and businesses need repairs as recovery shifts toward debris removal, rebuilding, and long-term housing. Authorities are also monitoring downstream flooding and a developing tropical system.

July 23

Catastrophe

Property

Risk Management

Texas

Texas, Louisiana Heat Wave Intensifies as Tropical Storm Bertha Raises Claims Risks

Tropical Storm Bertha is increasing humidity across Texas and Louisiana, driving heat index values as high as 120 degrees while record electricity demand and localized flooding threats create additional risks for property owners and insurers.

July 23

Catastrophe

Property

Risk Management

Alabama

Louisiana

Texas

New Leak Delays West Hollywood Water Main Repairs as LADWP Extends Sunset Boulevard Closure

Just as LADWP prepared to reopen Sunset Boulevard after replacing the ruptured 36-inch water main, crews discovered another leak that could extend repairs. The latest setback adds uncertainty for property owners, businesses, and insurance claims tied to the July 16 flooding.

July 23

Insurance Industry

Property

Risk Management

California

Florida Homeowners Insurance Lawsuits Drop to 41% of U.S. Total After Litigation Reforms

Florida's latest insurance market report shows litigation reforms continue to reduce homeowners insurance lawsuits, lower defense costs, improve insurer profitability, and shrink Citizens Property Insurance's policy count.

July 23

Insurance Industry

Legislation & Regulation

Litigation

Property

Florida